Just what Become familiar with

Are produced land, in earlier times entitled mobile property, has changed in the trailers of history on gorgeous and sensible options for of a lot homebuyers.

Having various have and designs, not only will they look identical to normal stick-built otherwise on-site belongings, however, the current are made property meet strict safety criteria, try energy-efficient, and can be obtained getting much less than simply traditional properties.

And you can sure, you can aquire home financing for your are formulated house. You should be aware that certain lenders prevent are designed house because they have emerged due to the fact an elevated risk. But great news-Atlantic Bay now offers investment to possess are manufactured property, and a single-time closing design-to-long lasting alternative. If you would like discover more about your options away from are produced home, our Mortgage Bankers are often ready to mention!

What exactly is a produced Home?

A created home is the newest U.S. Company from Casing and you may Development (HUD) term to possess property situated entirely inside the a manufacturer considering government HUD rules and transmitted on property to the a permanent material chassis that provide structural support adopting the residence is mounted on the website. Locate a home loan to your a made home, it should be real-estate, meaning its connected to belongings you possess otherwise rent, sleeps to the a permanent concrete foundation, and axles was indeed got rid of. Are produced belongings depreciate throughout the years.

Mobile residence is an obsolete label one to simply relates to belongings built in a manufacturing plant ahead of June fifteen, 1976, when HUD introduced the brand new Federal Are produced Homes Build and Shelter Requirements Act.

Standard land are produced house that are built in parts in the a factory, upcoming transferred and you can put together toward-webpages. They don’t have tires and are strung just as a conventional family. Hence, standard belongings take pleasure in or depreciate on the market identical to a good typical home.

On your own research, it’s also possible to discover the phrase prefabricated property. This is certainly an enthusiastic umbrella name which covers all kinds of home made in industries, including are formulated, modular, real, system, panelized, and you may log belongings.

The newest You.S. Census data shows that the typical price of a created house is around $88,100000. Your own residence’s rate will depend on a number of requirements. For example, you can find solitary-, double-, and multiple-broad floor arrangements available, also those services. Once the domestic must be affixed so you’re able to permanent assets, you will need to:

If you wish to get land and you can a freshly-depending household meanwhile, a greatest option is the only-go out closure structure-to-long lasting loan, and therefore brings together the development of one’s the fresh new were created home with the newest residential property purchase and you may permanent home loan into the just one closing, saving you fees.

Funding The Manufactured House

To shop for a manufactured home is maybe not rather than to invest in a motor vehicle. You can buy another domestic due to a retailer, buy a great made use of house, otherwise, in certain states, get directly from an owner. You can use a real estate agent to help you, just like a vintage home.

All of the old-fashioned financing applications has actually choices for are manufactured property since enough time because you fulfill the prerequisites. Including, your residence need to be at the least eight hundred sq ft and you can 12 feet wider, end up being connected to a long-term foundation, and can include very first have instance eating and you will asleep areas and you may sanitary facilities. Credit history conditions will vary, but 580-620 is a great rule of thumb. And when need assistance with their downpayment and closure can cost you, down-payment direction apps apply to are produced homes, too!

Pro Tip

Homeowner’s insurance having are created land will be more challenging to locate and you will is generally higher than compared to old-fashioned land. However, discover businesses that focus on insuring are built belongings. Look around to own rates as they can differ extensively.

Old-fashioned Financing

Having Fannie Mae’s MH Virtue program, your house need certainly to fulfill specific build, structural construction, and effort-results conditions, much like adhere-mainly based A traditional home built right on much, rather than are built property, which are built in factories and you can sent to the new lot. stick-established A timeless home built close to a lot, instead of are built homes, which are made in industrial facilities and sent to the brand new parcel. land. MH Virtue loans come with 31-year terms and you will down payments as little as step 3%.

Such Federal https://speedycashloan.net/loans/emergency-loans-no-credit-check/ national mortgage association, Freddie Mac’s House It is possible to funds bring repaired-speed mortgage loans from 15, 20 and you may three decades, adjustable-price mortgages, and you can an effective step 3% deposit. For those having solid borrowing, Freddie’s CHOICEHome program requires 5% off and will be used to your each other number 1 and you may second property.

Government-Supported Funds

FHA, Va, and USDA finance is a familiar financing choice for are produced property as their underwriting standards are more versatile than just one to off Conventional money.

FHA Name We loans funds the fresh are produced house one to normally arrive when you look at the are produced home organizations or parks. Your house need to be most of your house, while ought to provide a finalized lease for the lot with a first identity of at least 36 months.

Identity II money are accustomed to finance the house and land, and just due to the fact a primary residence. They may not be for leased spaces. FHA down money begin as little as step three.5%.

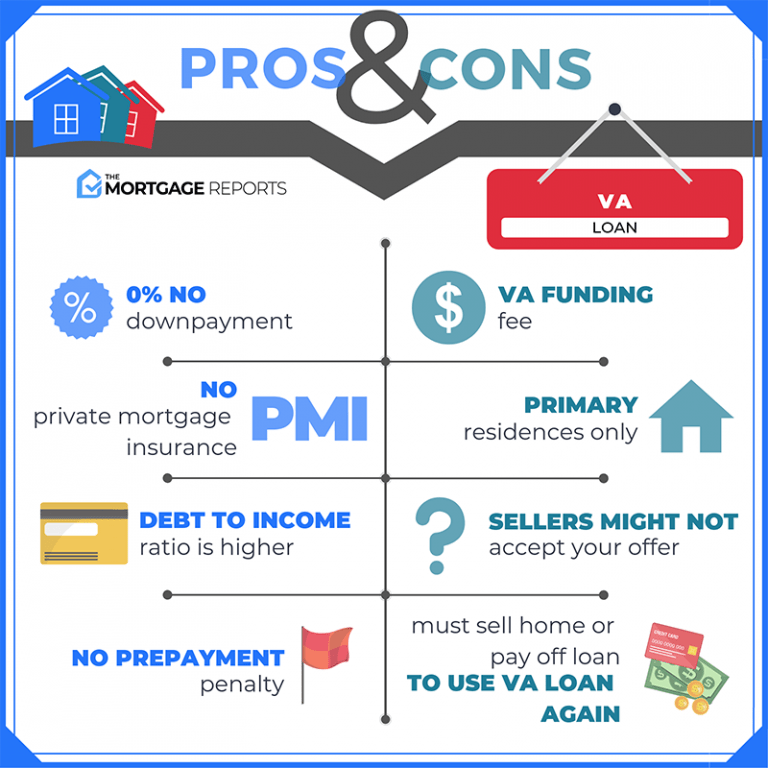

To possess services users in addition to their spouses, Virtual assistant financing cover are built property which have zero deposit. Even so they provides less regards to 15-25 years-definition you only pay more each month, but you’ll pay back the debt smaller. You must meet Virtual assistant are made household direction and supply a keen affidavit away from affixture to demonstrate the house are enhanced a house (houses). You could move your own Va investment percentage into the financing equilibrium.

Just like any USDA funds, you might funds their were created house with zero deposit. Although not, the home have to be brand name-brand new and you can twice-wider otherwise huge. You ought to see particular earnings restrictions, additionally the home need to be in the a location that suits USDA populace requirements.

Other Resource Choice

If all else fails, you can look at funding using your manufactured family broker, a consumer loan, or a beneficial chattel loan, that’s a unique loan to have high priced car such as for instance manufactured homes, airplanes, and you will farm gadgets. Costs for everybody of these finance is large, but there is smaller documents in the closing. Always check around before investing any sort of financial.

As you can see, you really have many choices to own investment a made domestic-you might just need to set up a little extra performs. However, contemplate, Atlantic Bay is always right here to greatly help!